Brittany Jones, Law & Public Policy Scholar, J.D. Anticipated May 2020

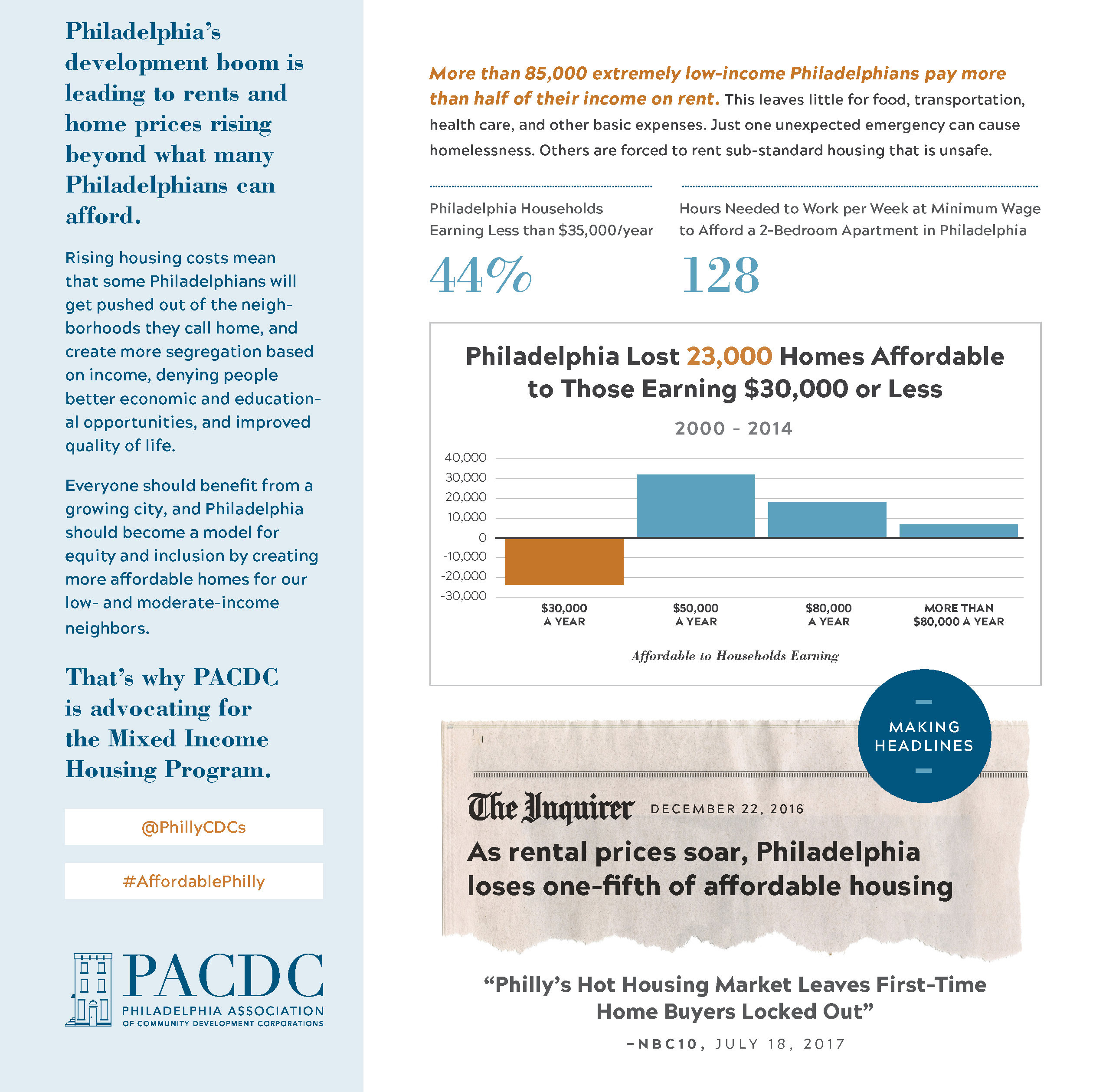

Philadelphia’s economy has been on the rise for the last twenty years. It now has one of the largest economies and hottest housing markets in the country, making it ideal for many young professionals. However, this economic change has left many members in the Philadelphia community behind. Rising housing prices have left more than 85,000 low-income Philadelphia residents having to spend more than half of their income on rent while over 23,000 houses available for residents earning $30,000 or less have disappeared between 2000 and 2014. At the same time, there are currently over 42,000 vacant properties within the city limits. In an attempt to address the growing number of blighted and debilitated vacant properties and lots, as well as affordable housing issues, City Council established the Land Bank in 2013.

{kind=link}

The Land Bank was an agency created to consolidate surpluses of public and private delinquent property and repurpose them for productive use by the community. However, since its inception, the Land Bank has been plagued by controversy. A series of scandals related to the distribution of property to politically connected buyers and improper use of property purchases has painted the program as a system designed to promote corruption and favoritism. In 2019, City Council passed legislation to create more transparency, oversight, and objectivity with the Land Bank process. One area addressed was the enforcement of purchase agreements. Initially, the Land Bank could monitor purchased property but had no manner of enforcing the conditions of the sale. Those aware of this loophole took advantage of the Land Bank’s system. An individual could purchase a vacant lot for well below market value by promising to create a community garden but then quickly turning around and selling the lot for new housing. Repeat stories of such purchases have led to growing public distrust of the Land Bank and its efforts.

In an attempt to combat these concerns, City Council’s legislation introduced sales conditions to purchase agreements such as deeds and covenants, as well as the right to repossess the property if agreement terms are not met. It also allowed the Land Bank to monitor its purchased properties for compliance. However, these reforms left more questions and ambiguity about the enforcement process than before.

Attached to its new legislation, City Council developed guidelines for the Land Bank’s acquisition and disposition policies. The acquisition and disposition process, by which the Land Bank obtains and distributes property, respectively, are two of the Land Bank’s three main operations. The new legislation treats the acquisition and disposition as the main process, and its investment in their policies and procedures reflects that. However, enforcement is a critical step that deserves similar treatment. The enforcement procedures for a program allow the agency to monitor the effectiveness of its work, as well as allowing for increased transparency in the program and fostering the public’s trust.

To prioritize the enforcement process, City Council should establish policy guidelines for it, just as it has done for acquisition and disposition. These guidelines should include definitions of all potential conditions that can be added to the purchase agreement, as well as clarification of the circumstances under which each condition can be added. This would promote clear communication and understanding between the purchaser and the Land Bank. A financial penalty should also be added. This penalty would be useful for purchase agreement violations where repossessing the property is not the most advantageous option for the Land Bank. It could be helpful in situations when repossessed property may be hard to sell again, such as those involving side yards that would only be useful to the adjacent property owners. A penalty of repossession could lead to a surplus of unloadable properties in the Land Bank. It might also be helpful developers who make large purchases and would have to return land in less-than-ideal conditions—making it once again harder for the Land Bank to find new owners. The funds collected from this penalty should go to the Housing Trust Fund, a fund that supports affordable housing in the city.

Under the new legislation, the Land Bank can monitor purchased property, but there are no clear guidelines for how it should go about doing so. Moreover, monitoring purchased lots would lead to a high financial and human cost for the agency. There are 2,200 properties within the Land Bank. Although a small number of properties have been distributed, it would be difficult to monitor properties throughout the City on a continual basis. To this end, City Council should consider establishing a formalized partnership with local community development centers (CDCs) to help with the monitoring process. CDCs are stakeholders that are deeply invested in the community and already would like an increased role in these affairs. Having established representatives in each neighborhood CDC would allow the Land Bank to have comprehensive monitoring reports for property within specific neighborhoods. It would also serve as another form of pressure on property owners to comply, as well as provide another instrument for transparency and public participation.

As the City of Philadelphia continues to address issues with housing shortages and vacant properties through the Land Bank, City Council should reform its enforcement of purchase agreements. A purchase agreement with no consequences prevents the Land Bank from reaching its goals and undermines its trust with the public. If the Land Bank wants to become an integral and productive part of the City’s efforts to revitalize neighborhoods, it must create clear enforcement guidelines and develop community buy-in through official partnerships with local CDCs.